Credit photo : European Commission

La note est aussi disponible en français ici

“Getting it right through time means that we perceive correctly changes in the human environment, incorporate those perception in our belief system, and alter the institutions accordingly…We tend to get it wrong when the accumulated experiences and beliefs derived from the past do not provide a correct guide for future decision making…And in cases where conflicting beliefs have evolved, the dominant organizations may view the necessary changes as a threat to their survival…(resulting in) an inability to make the necessary institutional changes” D. C. North, 2005, Understanding the Process of Economic Changes, Chap. 9.

The need for a strategic review of the European fiscal rules

The reform of the European fiscal rules (Stability and Growth Pact) is on the agenda. At the begin of 2020, the European commission is due to present a review of these rules and, possibly, make proposals to reform them. It will have not only to look backwards the years since the adoption of the legislation, the so called six- and two packs (2011 and 2013), but also to look forward anticipating what will be required to make the European Green Deal proposed by the new Commission a success. While the European Central Bank is engaging a strategic review of the monetary policy of the Euro area taking account of success and failures as well as of new challenges, it could not be understood that budgetary authorities do not start an in depth reflection putting the ecological transition in the center of their preoccupation. Indeed, even if European financing of the Deal via the budget or the European Investment Bank would increase beyond what looks at this stage politically within reach, there will still remain a need for mobilizing fund at national level either to complement European funding or in support of policies best designed and financed at a sub-European level.

There are basically three possible ways to adapt the rules to new circumstances and challenges. The first is to leave it to technical discussions among the sole Ministers of Finance and the Commission to adjust marginally the interpretation of the legislation as it was the case at some occasions since 2013[1]. The second is for the Commission to propose a reform of the legislative frame, the six- and two-pack, involving therefore the European Parliament and opening a public debate. The third would be a reform of the provision of the EU Treaties to adapt the rules imposing limits to the current deficit and the public debt to new circumstances. The choice can, however, only be made based on a substantial discussion on what change is needed.

The path towards the irrelevance of the present fiscal rules

The legislation of the fiscal rules, the so called six- and two pack, has been last reformed in 2011 and 2013 following the financial crisis. The objective was to ensure the credibility of the targeted stabilization or reduction of the public debt to GDP ratio that increased rapidly following the massive fiscal impulse of the crisis years 2009/10. The interpretation of the Treaty provisions that the public deficit shall not exceed 3% of GDP and the public debt shall be less that 60% of GDP was therefore restrictive. It imposes in particular that the deficit fluctuates during the economic cycle around a level at the equilibrium or near to as to minimize the risk that the limit of 3% of GDP is exceeded. Is the debt greater that 60% the provision is even more restrictive.

There are two substantial reasons why an in-depth reflection on the European fiscal rules need to be engaged.

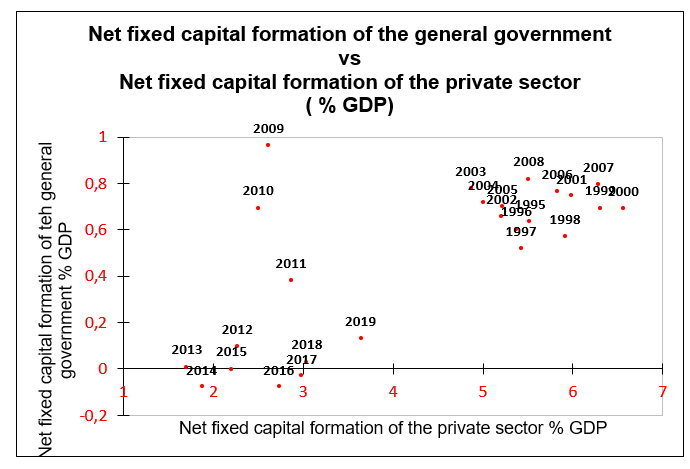

The first reason is that the macroeconomic context has profoundly evolved over the last decade. Interest rates came down and the real cost of indebtedness – the interest rate after deduction of the inflation rate – is negative in several countries while it reached around 3% on average of the Euro countries at the begin of last decade. As explained by O. Blanchard, this substantially changes the way we have to look at public debt. On average of the Euro countries the public deficit is about 1% of GDP against 6% at the begin of 2010. All countries show a deficit at or well below 3%. The public debt/GDP ratio is declining in most countries or stabilized, in some cases at a level well above the limit of 60%. However, it should be recognized that this limit was fixed 30 years ago under specific circumstances (P.5) and is largely arbitrary, as recognized by the European Fiscal Board (EFB) in a recent report (P. 92). Further imbalances persist or have been aggravated. External accounts diverge among EU economies. Regional and social inequalities have increased. Net public and private investment are downsized in Europe while the euro countries achieve a sizeable external surplus invested abroad. The European Central Bank (ECB) and other international institutions warn that the capacity of monetary policy to support economic activities is vanishing and call for a greater support by economic and budgetary policy. For these facts alone, a strategic review of the European budgetary rules is urgently needed, as the ECB intends to do it for its own monetary policy.

There is a second, even more fundamental reason for such a review. The principles of the economic policy coordination need to be put in conformity with the European Green Deal, as it has to be the case for any other European policy. The need for coordination and cooperation goes well beyond what it was the case until now. It reaches out fiscal issues (corporate and energy) as well as subsidies (carbon). Investment needs in key sectors (building insulation, transport, energy) to meet climate goals have been estimated at around 260 billion a year (around 1,7 of GDP) by the European Commission. National budgets will have to come in on top of private and European financing. Further pressures will be put on public expenditures, for example, to support innovative technologies, accompanying the transformation of most affected sectors or regions, adapting our societies and economies to the climate change, compensating most vulnerable for the increase of carbon taxes.

The inconsistency of the fiscal rules with the European Green Deal

Member States will commit themselves on medium term policies to meet climate targets in the National Energy and Climate Plans. The final version shall be adopted at the very begin of 2020. The consistency of the budgetary policy with these commitments will be decisive for the success of the transition.

However, this consistency is endangered by the fiscal rules:

- The rules focus on an (arbitrary level) of public debt to GDP ratio. On top, the unicity of the target is inconsistent with the heterogeneity of the countries (see the report by the EFB, P. 92). Most important, the rules only marginally take account of the increased need for investment and public expenditures with an high expected return to fight climate change. Not acting and not investing today, is taking the high risk of a fall of the production and of irreversible damages tomorrow. In other words, the rules consider only one side of the medail, the debt, but not the assets or public capital. It is even more urgent to invest today that the cost of debt is near to zero or even negative in some countries. Those in favor of the statute quo argue that sufficient flexibility is granted under the existing rules. But those clauses neither refer to the different indebtedness capacity of countries nor to the return of expenditures related to the fight of climate change.

- The implementation of the rules substantially relies on a non-observable variable, the “potential output” (or potential GDP), calculated on the base of a theoretical model. This calculation is contestable and contested and, as a consequence, so the policy recommendations based on it. The starting point of the reasoning is that the fiscal receipts (and some expenditures) fluctuate with the GDP. In good times, fiscal receipt are flowing at a pace above what can be expected over the cycle; therefore, the deficit is temporarily reduced. By contrast, in bad times fiscal receipts recess and increase temporarily the deficit. The elimination of this impact of the cycle on the deficit leads to the calculation of the “structural deficit”. This is this “structural deficit” that is targeted by the European fiscal rule. In bad times, because the “structural” deficit is smaller than the observed, the adjustment required by the rule will be less pronounced than if based on the observed. This way, there will be a positive impact on global demand as desired in bad times. And the contrary will be true in good times. So far, so good: – theoretically, such a policy has a desirable counter cyclical impact. But, how do we know if and how far the economy is in “bad” or “good” times? The answer under the rules is to calculate the gap between the observed GDP and the “potential output”, i.e. the notional output that is possible using available resources, the stock of capital and labor forces, without exercising inflationary pressures. Given this definition, it is understandable that the calculation of the “notional” output is contestable and contested: how to estimate the production function (the relation between the output on the one side and the stock of capital and the labor force, on the other), how to define the available labor force and to estimate the capital stock, what are acceptable inflationary pressures,…? The EFB noted in its report (P. 85): “Meticulous work on estimating the output gap has been going on for two decades in the Commission and among national experts,…. Nevertheless, significant revisions continue to be made, and major errors of judgement have been observed in policy recommendations in either direction..”. Wrong judgement not only undermines trust in a procedure touching the core of economic and social policies of the member states. It may also have concrete, damageable stop and go affecting in particular investment expenditures. This is particularly detrimental in the perspective of the energy transition requiring lasting investment efforts that should not be subject to the hazard of a weak calculation method.

- Even more fundamentally, the concept of a “potential output” dependent only on the capital stock and labor force does not meet the challenge in the present context. It neither takes in consideration energy as an ingredient sine qua non of the production, nor the physical and biophysical limits to the development of economic activities. It ignores the risk of break down and of an accelerated obsolescence of the capital stock as a consequence of climate change and climate change policies. However, exactly those risks and limits need now to be integrated while designing policies, including macroeconomic policies[2]. This is not without operational consequences. Flexibility clauses under the European fiscal rules allow under certain circumstances for the deduction of certain priority expenditures from the deficit. According to the present rules, the deductible expenditures have to support policies increasing the potential output. Now it’s time to prioritize expenditures in support of climate change attenuation and mitigation as well of biodiversity to protect our economies from climate hazard and massive shocks and to preserve an hospitable planet.

- The coordination of fiscal policies is perceived as necessary to preserve the common good “financial stability”. The common goods “climate” and “biodiversity” need now to be added. The sustainability of cooperation managing common goods depend not only on the adequation of the means to the end, but also on the balance between rights and duties, cost and benefit for each stakeholder and on the possibility to renegotiate those as the context evolves[3]. The above-mentioned report of the EFB underlines the unbalance between rights and obligations of the various countries of the Eurozone. While restrictive policies are required from countries with a debt ratio above limits, countries with a low debt ratio are not committed to expansive policies. The consequence is a deflationary bias. P. Gentiloni, the new European commissar for economy and finance made recently the point at a conference at the ECB, underlining that this is particularly detrimental in the context of low inflation and growth while the impact of monetary policy is running out (Financial Times 19th December). For the European Fiscal Board, this asymmetry together with the unicity of the debt target for all countries has a consequence: the concept of the stance of the aggregated fiscal policy for the euro zone as a whole lacks of operationality despite its high relevance in an economic and monetary union. Furthermore, the risk is to entrench underinvestment.

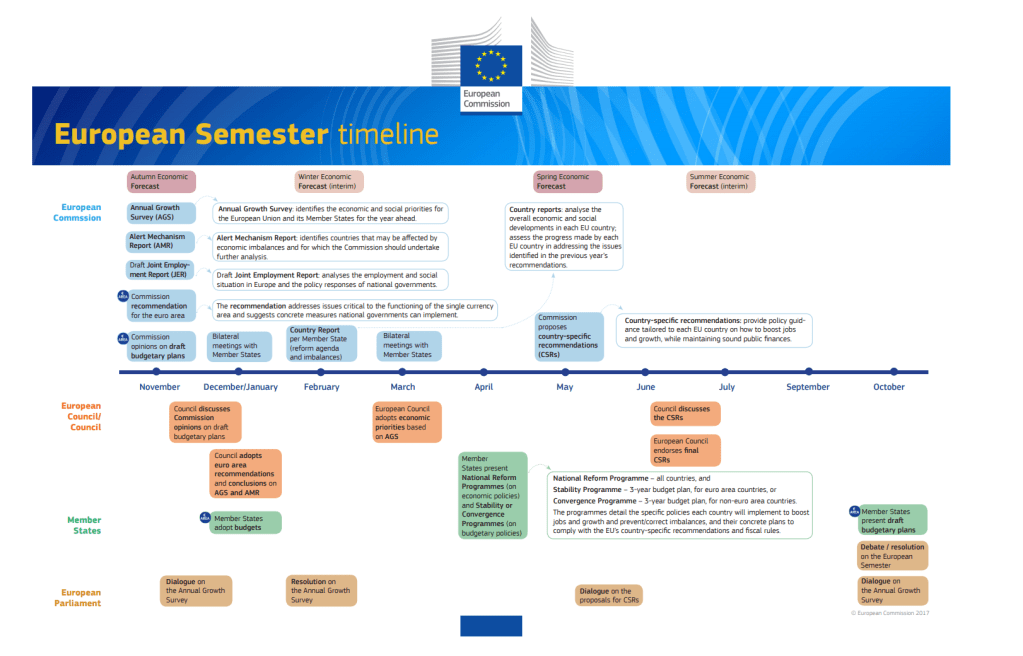

The European surveillance of public budgets is the hard core of the European Semester, an annual process coordinating national economic policies from November/December of a given year until end June of next year. This coordination addresses a very broad spectrum of economic, social, financial and fiscal policies. It leads to specific country recommendations at the end of the first semester of each year. The Commission von der Leyen has launched on 17th December the European Semester 2019/20. The new ambition is to integrate in the analysis the UN Sustainable Development Goals (SDG). Consequently, and for the first time this year, the need for a reinforced and coordinated investment strategy is underlined in the recital of the recommendation for the economic policy of the euro area (Par. 5) as well as in the background document. However, the recommendation stricto sensu does reflect only marginally this need (P. 7) and no link is established with the recommendation for the debt strategy. Indeed, as it is constrained by the rule and its dominant interpretation, the recommendation for the debt strategy is nearly unchanged compared to previous year:

- Full respect of the Stability and Growth Pact,

- The euro area fiscal stance is expected to be broadly neutral to slightly expansionary in 2020 and 2021

- At the same time, national fiscal policies remain insufficiently differentiated in light of the available fiscal space in Member States: in Member States with high debt levels, pursue prudent policies to put public debt credibly on a sustainable downward path. In Member States with a favourable fiscal position, use it to further boost high-quality investments

- In case of a worsening outlook, deliver a supportive fiscal stance at the aggregate level, while pursuing policies in full respect of the Stability and Growth Pact, taking into account country specific circumstances and avoiding pro-cyclicality to the extent possible

The very relevant recommendation of an increase of investment contrasts with the highly prudent and neutral recommendation for the debt. This inconsistency can only be solved with a reform of the stability and growth pact.

Two options for reforming the European fiscal rules

The EFB has made two reform proposals that can serve as a point of departure for this discussion. However, they have to be complemented to also take into account the public spending priorities related to the fight against climate change and the ecological transition.

The first option, and the less ambitious one, would continue to impose a progressive reduction of the public debt ratio for those countries with a level above 60%. However, the instrumental rule will be changed and simplified. It will no longer be based on the dubious calculation of a structural deficit. Instead, a limit would be imposed on the growth of non-interest expenditures, after deduction of unemployment expenditures and net of new measures affecting the revenues. This limit would be calculated ensuring consistency between the GDP growth trend – as a proxy for the organic growth of tax revenues – and the desired reduction of the debt ratio. A flexibility clause would be introduced but its activation would depend on an independent economic view and not on further sensitive and complex calculations. According to the EFB, this view would have to balance in bad times the deficit reduction needs with the short term negative macroeconomic impact of lower net expenditures (p.89).

In the same vein, the EFB suggests a reform of flexibility clauses whereby a Golden Rule would be introduced for certain investments or expenditures, allowing for a more generous definition of deductible expenditures. According to the EFB, this should cover in particular expenditures reinforcing growth factors and supporting programs financed by EU funds. However, this does not appear to be sufficient to fully take into account the needs under the European Green Deal. What is required is to favour the expenditures supporting sectoral policies for climate change mitigation and transition foreseen by the National Energy and Climate Plans. In this context the (currently restrictive and rigid) activation conditions for the flexibility clauses should be revised. For instance, the conditions could be replaced by a mutual agreement among European partners, taking into account on a country-by-country basis the interest rates, the level of “green” investments needed, their expected social and environmental benefits, and the duration of the investments. This would provide each country with an ‘expense envelope’ excluded from the deficit calculation which could be used for priority expenditures, allowing for an arbitrage balancing the cost of accrued debt versus the cost of inaction against climate change.

The second option proposed by the EFB is much more ambitious because it addresses the asymmetry of the obligations of countries with low versus high debt ratios. Each country would have public debt and expenditure targets adapted to its particular situation. According to the proposal, those countries with low public debt ratios would be committed to bolster growth factors, while those with a (too) high debt ratio would aim to reduce the latter. In addition, this proposal should be amended with a clause to favor investments in the ecological transition. This ambitious approach would also be a good opportunity to reflect further on economic policy objectives, considering alternative indicators to production which take into account the sustainability, wellbeing and environmental perspectives.

What are the next steps?

The experience of the past decade, the Commission’s new approach to the European Semester and the European Green Deal, all point to a revision of the Stability and Growth Pact. The goal should be to develop an approach which (1) fully takes into account investment needs and the cost of inaction, (2) is clearly linked to transition objectives and to the European energy and climate governance, particularly to the NECPs and (3) contributes to the consistency and complementarity of funding at the national and European levels.

Settling for an interpretation of the existing legislation by ministers of finance and the European Commission instead of reviewing the legislation itself would be a minimalist solution, likely doomed to fail.

The best option would be for the Commission to engage a public discussion and the European Parliament and to propose a revision of the directives and regulations relating to the SGP (six and two pack). The previous revisions of the secondary legislation and the jurisprudence have shown that there is considerable room for interpreting the European Treaties on these issues; this margin should be used to adapt the rules to current priorities.

Modifying the Treaty would entail heavy ratification procedures in all Member States. This may appears opportune later when the needed consensus on climate emergency and paradigm shift will have been consolidated.

[1] The interpretation of the rules is documented in two documents: Vade Me Cum on the Stability and Growth Pact (108 pages) and a compendium The Macroeconomic Imbalance Procedure (126 pages)

[2] See the literature reviews by the IMF and the Bank of England

[3] See the work of E. Ostrom on the management of common goods.

[…] in 2019, we have been working (see for instance, Game-changer: Financing the European Green Deal or European Semester, fiscal rules and the European Green Deal) on all the themes of the letter to the leaders of the Union in close cooperation with other […]

J’aimeJ’aime