Ollivier Bodin

In a note published in April, we called for a fund of 2,000 billion euros over 7 years to help all EU Member States cope with the economic crisis we are going through. The very path out of the economic crisis remains uncertain as it still depends on the possibility of a second wave of COVID in Europe and the evolution of the pandemic among the Union’s economic partners, particularly in America and Africa.

The pandemic has accelerated the growing awareness that the economic and fiscal policy instruments available at the European level are insufficient or inadequate to govern an integrated market with harmonised rules. Restrictions on free movement have been placed in a more or less orderly manner, common rules have been lifted, new Community programmes have been proposed and partly already adopted, old ones have been adapted, existing financial instruments are being adapted and new ones have been proposed (European Commission).

The Recovery and Resilience Facility proposed by the Commission is the major innovation of the recovery plan adopted on 27 May. It is threefold innovative in its structure: it will be refinanced by a European Union loan; it will involve a redistribution of resources between Member States; and it will be a financial incentive for countries to align their policies, investments and reforms with the objectives of the European Union.

According to the draft regulation (COM2020/408) the Facility amounts to 560 billion euros and will consist mainly (330 billion euros) of non-refundable financial support. The instalments of support will be linked to progress made in implementing national investment and reform plans, which will have to be approved in advance by the Commission. If necessary, these grants may be supplemented by a loan. The country will then benefit from the EU’s borrowing conditions. The implementation of the Facility will be anchored in the ‘European Semester’, the process of coordinating the economic policies of the Member States.

What is the logic behind this Facility?

The European economies will not re-start on their own. The effects of the pandemic and of the lockdown are only gradually diminishing. The pandemic is far from being over among the Union’s trading partners. Unemployment is going to be very high. Several enterprises will have significant tax (and social) debts and will have difficulty meeting their financial commitments with risks of many bankruptcies.

States must therefore intervene to prevent a deflationary spiral from taking place. But the intensity of the intervention required in a country often exceeds that country’s capacity to intervene. Without solidarity, necessary interventions would have to be abandoned, threatening the Union with economic, social and ultimately political disruption. Last but not least, it is essential that recovery plans are coordinated so that they contribute to the European Green Pact and that the urgency of recovery is not an excuse to delay the response to the demand for the fight against climate change.

In this context, the governance of the Facility seems to meet the need for efficiency and agility. Especially in the post-COVID recovery phase, commitments must address gaps that are uncertain in their nature and size and which can be better identified at national and even sub-national levels. But this also applies to many investments needed for the ecological transition. Such investments must be identified by a bottom-up process with margins for « trial and error ». These investments must also be accompanied by regulatory or tax measures to be effective. For example, the shift of urban mobility to low-carbon modes of transport will have to be done according to the preferences of the inhabitants. It will be the result of a set of measures including the nature of infrastructure (bike paths and/or charging stations), but also public transport pricing, taxation on fossil fuels, and so on. To speed up the proper insulation of housing, policies combining regulation, financial aid and professional skills development will be needed.

The decentralised governance of the measures supported by the Facility has the potential to respond to the macroeconomic emergency while steering in the right direction in line with European strategic objectives.

What are the limitations of this Facility?

The first limitation is the ability of the European Semester, and therefore national economic policies, to evolve in the direction announced by the Commission, i.e. with a focus on sustainable development targets. It will be necessary to give meaning and substance to the new metaphors of the European Semester, from « competitive sustainability » to the « first mover advantage » through the « just transition » (see for example COM-2020-500, P.7). And choices will have to be made. This includes focusing economic policies not just on indicators of financial imbalances, as is currently the case, but also on social and environmental indicators. Institutional reforms are also necessary to strengthen public policies; for example in the area of taxation through decision-making in the European Union by qualified majority instead of unanimity; in the area of revenue policy through the adoption of a European minimum income scheme; or through a prudential regulation, which accelerates the deleveraging of financial institutions in fossil fuel-dependent sectors. The fact that the proposed regulation of the Facility puts as a first criterion for evaluation the ability to « boost potential growth », a widely disputed concept, suggests that we are still far away to replace the old productivism paradigm with one of sustainability.

The second limitation is the governance, which is essentially based on a dialogue between the Commission and national authorities. The draft regulation does not provide for prior consultation with the European Parliament on the national recovery and resilience plan that will form the basis of funding. Nor does it provide for any consultation with civil society or social partners. One understands the concern to avoid a « Christmas tree » effect where each actor would have the opportunity to add « his » priority and the consistency, and therefore the effectiveness of the plan, could be at risk. Nevertheless the effectiveness of the Facility will be improved if the Commission and national authorities take account of the views of diverse stakeholders while elaborating the national recovery an resilience Plans to be funded, and at the same time strictly limiting them to concrete, precise and specific objectives. The draft regulation should be enhanced in both those dimensions during the negotiations in the Parliament and the Council.

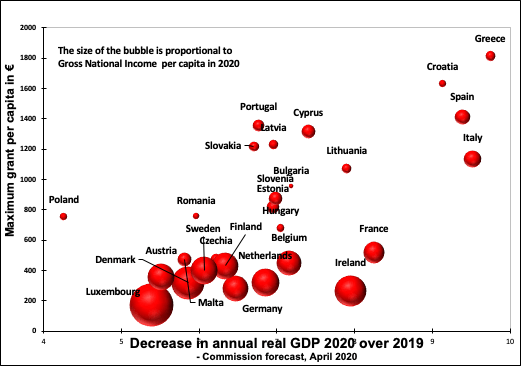

The third limitation is related to the size of the Facility. The amount itself represents on average only slightly less than 1% of GDP per year for 3 years, while the fall in GDP this year alone in the EU countries is estimated at 8% to 12% (depending on the country) and uncertainties weigh on the speed of recovery.

The Facility may nevertheless have a significant macro-economic impact in some countries because it is highly re-distributive (see charts below). The Commission has used a formula whereby the maximum amount of support per capita is linked to the magnitude of the impact of the crisis and the level of the national income per capita. For the most affected countries with the lowest per capita income, transfers will range from 12 to 14% of GDP over three years. Spain and Italy, two heavily affected countries with per capita income below but close to the European average, will be able to receive sufficient grants to considerably relax their constraints on public spending.

However, the Facility in itself will not solve the systemic problem of fiscal policy coordination in the euro area.

Public debt ratios will rise sharply in virtually all countries, beyond the Treaty limits of 3% current account deficit and 60% debt as a share of GDP. For the time being, the Stability Pact’s budget rules have been suspended, but this is temporary. One way or another, fiscal policies will have to be coordinated.

Before the pandemic, the Commission had launched a consultation on a reform of budgetary rules that was due to end on 30 June. It will now probably have to be relaunched to reflect recent experiences. Many proposals are on the table. The chosen reform will have to solve, in particular, three problems:

- Taking into account a profoundly changed macroeconomic context in which the thresholds selected more than thirty years ago in the Treaty no longer make economic or financial sense;

- Breaking out of the asymmetry whereby countries with a fiscal deficit face budgetary restrictions, while surplus countries are not in turn incentivised toward fiscal expansion. This is not only a matter of fairness, but also necessary to remove the deflationary bias of the current rules;

- Setting a golden rule that recognizes the unquantifiable but absolute top priority of expenditures supporting the green transition.

The fourth limitation is related to the three-year term of the Facility. The ecological transition is a long-term process that will continue beyond 2030. All countries and investors must be able to commit to it with the greatest certainty possible about long-term financing resources. However, it is unlikely that by the end of 2024, the divergences between countries will have sufficiently narrowed to render the solidarity effort unnecessary. The challenge will then be to invest in the ecological transition, a common good of all Europeans, with equal intensity in all countries.

The financing of the Facility through a community loan can also serve integration. It is legitimate as a contribution to short-term macroeconomic stabilization and as a source of long-term, high-return ecological financing and investment. This common borrowing should also provide a strong incentive to increase the Community budget’s own resources, particularly through specific European taxes, such as a corporate tax, financial transactions tax and a carbon tax at the borders, which would prevent the solidarity effort from being carried out mainly through transfers between states.

For the time being, the Community budget funds or co-finances projects of common interest, such as external border protection, research programmes, cross-border infrastructure, and regional development. To this first pillar, the Facility would add a second pillar, frequently met in budgets of federation of states: solidarity funding for expenditure of common interest, but identified and implemented better within the framework of national or sub-national policies. Let’s hope that this opportunity to make a step towards a better functioning Union will not be missed.

Available in pdf here